Week Ahead & Technical Analysis: Week 45, 2025、

(USD/CAD | AUD/USD | WTI Crude)

Welcome to your weekly edge in the markets with clear, actionable insights.

It’s split into two parts:

1. Week Ahead – An overview of current market conditions, previewing the week ahead.

2. Technical Analysis – our top 3 trade ideas for the week, complete with charts and key levels to watch.

Week Ahead

10–16 November, 2025

Global markets enter mid-November with sentiment fragile after a tech-led pullback knocked the S&P 500 off record highs and alternative private data muddied the US growth picture during the government shutdown. Focus turns to a UK data barrage, China prints, and a dense slate of UK corporates, with the Fed’s December path in play as pricing implies a ~65% chance of another cut.

Week in Review

News

Central banks steady the course:

The Bank of England kept rates on hold with a close split that underscored a live debate on cuts. The RBA also held and sounded cautiously hawkish. Fed Chair Powell, after October’s 25bp cut and QT wind-down signal, warned that another December cut is not a given, keeping rate expectations fluid.

US data vacuum and shutdown effects:

With official US releases delayed, investors leaned on private gauges: ADP showed +42k jobs in October, while Challenger announced 153k planned layoffs, and the Chicago Fed estimated unemployment at a four-year high.

Earnings pulse remains strong:

Despite the wobble in equities, US Q3 reporting stayed robust: with 446 S&P 500 companies out, 82.5% beat estimates, the best since Q2 2021.

Price Action

Equities:

The S&P 500 fell for the week, now ~2.4% below its 28 October closing high. Tech led the drawdown, with the S&P tech sector down ~6% on the week, while the FTSE 100 held firmer on sterling softness.

Commodities:

Oil eased after US inventory builds and OPEC+ chatter on output. Gold stabilised after a 10% correction from records, with dip-buying evident as yields cooled.

FX:

GBPUSD faded towards 1.30 on BOE-vs-Fed dynamics. The yen outperformed on risk aversion. NZD lagged amid softer domestic signals.

Big Themes

Equity leadership narrowed as AI-linked names corrected, raising questions over stretched valuations after a 35% S&P 500 rally since April. Gold’s drawdown mirrors reduced hedge demand, while a weaker pound has aided FTSE 100 exporters. Crypto remains heavy after October’s liquidation shock, with key resistance still capping rebounds.

Week Ahead

Earnings Calendar

Vodafone (H1 FY26) – Monday, 11 Nov:

Modest recovery from multi-decade lows. Watch German turnaround, synergy delivery from the Three merger, and confirmation of FY26 guidance (underlying cash profits €11–€11.3bn; FCF €2.6–€2.8bn). €500m buyback in focus.

Cisco (Q1 FY26) – Wednesday, 12 Nov:

Cisco reports amid volatility in tech. Last quarter revenue fell 3% to $13.5bn, with software and security offsetting weaker hardware demand. Focus on AI-driven data-centre orders and signs of a second-half rebound.

Rolls-Royce (Q3 FY25) – Thursday, 13 Nov:

Shares near record highs ~1,200p. H1 underlying op profit +50% to £1.7bn; FCF £1.6bn; guidance raised. Civil aero margin ~25% the engine. SMR funding plans remain a watchpoint; IPO talk denied.

Burberry (H1 FY26) – Thursday, 13 Nov:

Turnaround under “Burberry Forward” targeting £80m savings. Q1 revenue -6% to £433m; Asia soft, US +4%. Evidence of margin traction and brand momentum in focus.

Disney (Q4 FY25) – Thursday, 13 Nov:

Parks and cruises strong; content softer. Q3 EPS $1.61; Disney+ +1.8m subs. Watch cost discipline and franchise slate guidance.

Economic Calendar

UK Wages/Unemployment (Sep) – Tuesday, 11 Nov:

Jobless rate has risen from 4.0% to 4.7% y/y; wage growth holding ~4.7% with public-sector strength. Sticky pay keeps BOE constrained ahead of the Budget and amid IMF warnings on UK living standards.

UK GDP (Q3) – Thursday, 13 Nov:

Monthly GDP +0.1% in August after a -0.1% July revision; services flat. Manufacturing/industrial gains may support Q3, but momentum remains fragile.

China CPI (Oct) – Sunday, 10 Nov:

Seen slipping back into deflation around -0.1% y/y, raising stimulus hopes.

China Retail Sales (Oct) – Friday, 14 Nov:

Seen easing to ~2.2% y/y from 3.0%, implying softer consumption.

Australia Unemployment (Oct) – Thursday, 13 Nov:

Tight but cooling labour market as RBA stays cautious.

EU GDP (Q3, 2nd) – Friday, 14 Nov:

Confirms modest growth amid weak manufacturing.

US data note:

CPI, PPI and Retail Sales are likely to be delayed by the shutdown.

Technical Analysis

We look at hundreds of charts each week and present you with three of our favourite setups and signals.

USD/CAD

Setup

Bullish breakout

- Completed an inverse H&S bottom

- Broken above 1.40 but not cleared 1.41

- Daily moving averages in bullish alignment

Commentary

Despite the highest weekly close in months, there was hesitation at 1.41 - offering the chance for a pullback trade.

Strategy

- Buy pullback near 1.40

- A close below 1.39 would indicate a deeper correction

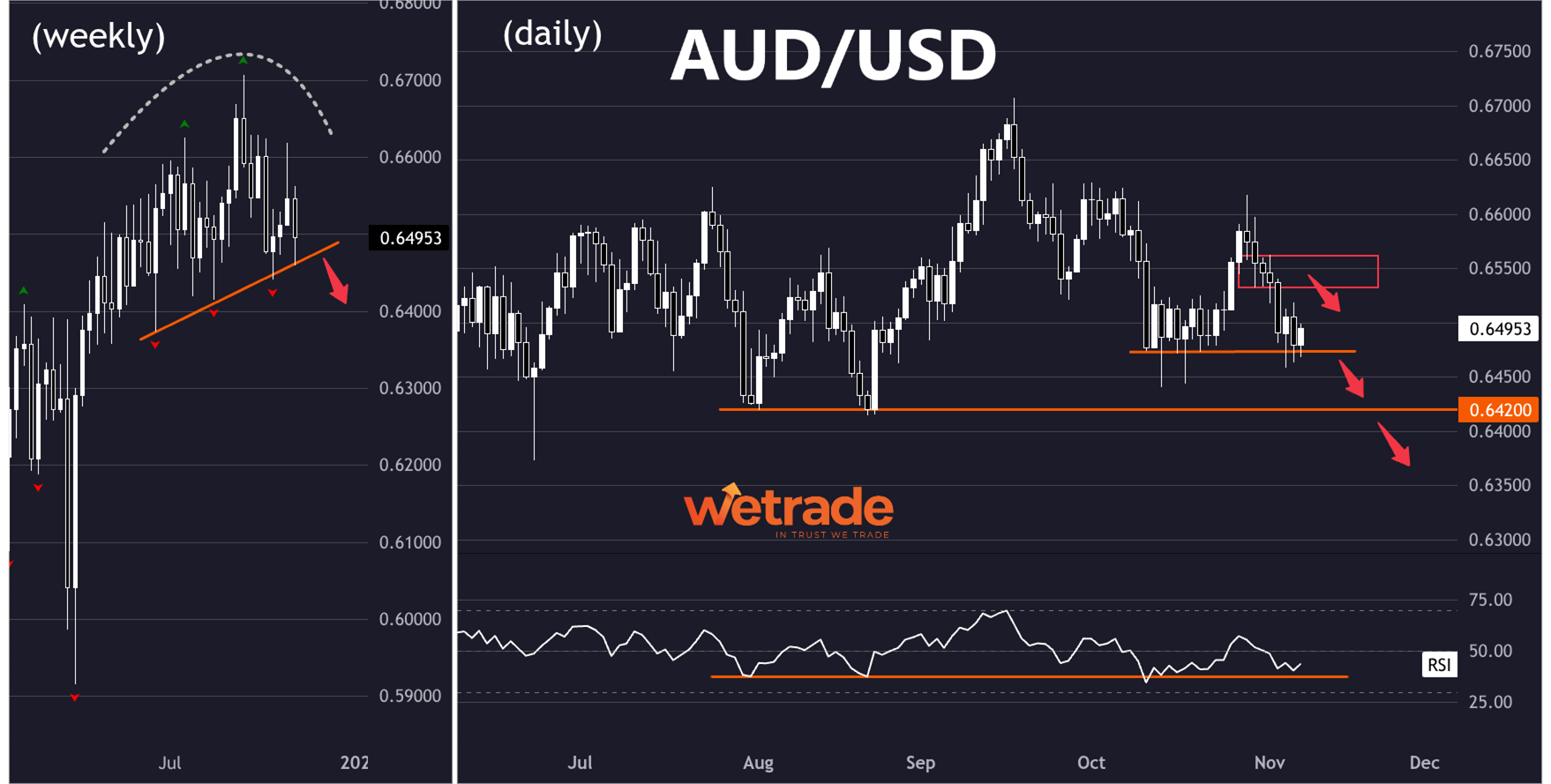

AUD/USD

Setup

Range market - possible bearish reversal

- Need a break of the weekly uptrend line to turn bearish

- Solid support from 0.64-0.65

Commentary

The weekly price action looks more like a top than a continuation. Our bias is towards a bearish break, but we will be cautious about any bearish trades before support breaks.

NOTE: Look out for bullish reversal from 0.64 (bottom of the range)

Strategy

- Look for bearish setups after a close below 0.65

- Buy if there is a strong move off support at 64

WTI Crude Oil

Setup

Bullish reversal off long-term support

- Bullish engulfing weekly candle off 56.0 support

- Daily trend is still down - looking for bullish break

Commentary

Looking to trade in line with signs of new bullish momentum. A close above 62 (support-turned resistance) would confirm a new bullish bias.

Strategy

- Aggressive: Buy bull flag breakout

- Conservative: Wait for bullish setups after break over 62

But - as always - that’s just how the team and I are seeing things, what do you think?

Share your ideas

OR

Send us a request!

Cheers,

Jasper

Disclaimer:

The communication does not constitute investment or trading advice, nor does it include any recommendations. Additionally, it does not serve as an offer or solicitation to engage in transactions involving financial instruments. WeTrade does not take responsibility for any actions taken based on the information provided, nor for any outcomes that may occur as a result of the actions taken.